Dear PGM Capital Blog reader,

In this weekend blog edition, we want to discuss the Q4- and full FY-2019 financial reports of Chinese Refiner SINOPEC and Dutch-Belgium Food retailer Ahold-Delhaize.

SINOPEC’S FY-2018 FINANCIAL REPORT:

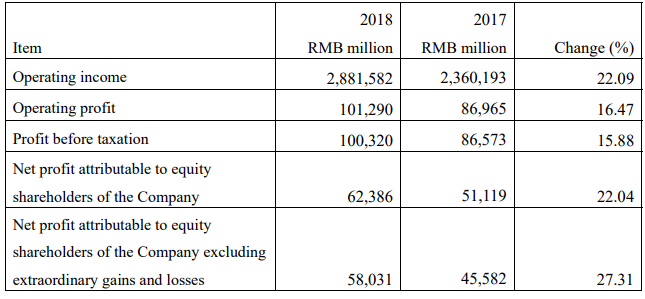

On Friday, January 25, 2019, China Petrochemical Corporation (Sinopec) (0386.HK), China’s largest oil refiner, announced its preliminary financial data for 2018 as follows:

As can be seen from above table containing the preliminary earnings estimates filed with the Shanghai Stock Exchange, the company’s revenue increased by 22.09 percent year on year to 2.88 trillion yuan. While its operating profit increased with 15.88 percent compared with FY-2017.

AHOLD-DELHAIZE Q4-2018 FINANCIAL RESULTS:

On Wednesday January 23rd, Ahold Delhaize (AD.AS), the Dutch-Belgian supermarket operator, reported its Q4-2018, financial results with the following highlights:

- Net sales of €16.5 billion, up 3.0% at constant exchange rates

- Comparable sales* in the U.S. up 2.7%, showing continued good momentum

- The Netherlands comparable sales up 3.3%, cycling a strong fourth quarter 2017

- Ongoing operational improvements in Belgium resulted in 3.0% comparable sales growth

- Central and Southeastern Europe comparable sales* up 2.0%, with strong sales in the Czech Republic

- Net consumer online sales up 26.4% at constant exchange rates in the fourth quarter and

reached €3.5 billion for the full year 2018.

Overall the business delivered another strong sales performance in the fourth quarter and for the full year 2018. For the full year, net sales reached €62.8 billion, up 2.5% at constant exchange rates.

Sales performance in the United States continued to show good momentum with 2.7% comparable sales growth excluding gasoline in the fourth quarter.

The Netherlands had a solid performance with 3.3% comparable sales growth compared to a strong fourth quarter last year.

In Belgium the implementation of the strategic plans to improve the operational performance of the Delhaize stores is reflected by a comparable sales growth of 3.0% for the fourth quarter of 2018.

In Central and Southeastern Europe comparable sales grew by 2.0% excluding gasoline.

PGM CAPITAL’s ANALYSIS & COMMENTS:

Sinopec:

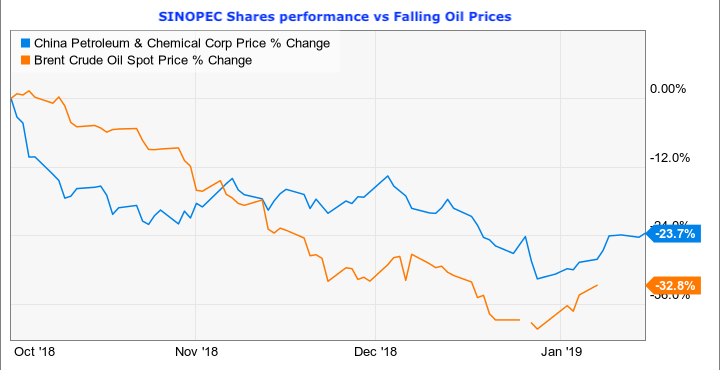

SINOPEC, focused on the Chinese market, is a diversified oil and natural gas company, with upstream (drilling) and downstream (chemicals and refining) operations. Of course, volatile oil prices often impact the energy concern’s top and bottom lines. That helps explain the steep drop in the stock’s price in recent months as oil prices fell. But that could be an opportunity for investors interested in China, since the company is still set to benefit from growth in its core market.

As can be seen from below chart, since early November, the shares of SINOPEC, have outperformed the Oil price which can be seen as very bullish.

China is an important growth market for many industries, notably energy. As the country continues to grow, increasing energy demand will be the norm.

To put a different spin on that, China is the world’s largest car market and SINOPEC is a key fuel supplier. Yes, car sales have fallen recently, which suggests the market is maturing, but that doesn’t change the still-huge need for gasoline: Third quarter gasoline production was up 7% year over year. And that’s just one business. For example, chemicals are also seeing increasing demand as the nation industrializes, with the company’s volumes advancing 12% year over year in the third quarter.

If you are interested in China because of its still relatively strong growth prospects, then you should look at SINOPEC. The oil price decline that fueled the stock’s recent drop, meanwhile, simply made the shares that much more interesting.

If you are interested in China because of its still relatively strong growth prospects, then you should look at SINOPEC. The oil price decline that fueled the stock’s recent drop, meanwhile, simply made the shares that much more interesting.

Based on the above mentioned fundamentals, with a P/E ratio of 12, strong balance sheet and a dividend yield of 9.5 percent we maintain our STRONG BUY rating on the shares of SINOPEC.

Ahold-Delhaize:

During the presentation of the Q4-2018 figures, they said that for the full year 2018, they expect underlying earnings per share from continuing operations to be at the higher end of their previous guidance of €1.50-1.60.

Full year free cash flow is expected to be more than €2.0 billion, supported by further improvements in net working capital. Capital expenditure for 2018 is expected to be €1.8 billion, in line with previous guidance.

As can be seen from below chart, shares of the company, have appreciated with approx. 30 percent during the past 52 weeks.

Shares Buyback Program:

Ahold Delhaize has repurchased 1,116,700 of Ahold Delhaize common shares in the period from January 14, 2019 up to and including January 18, 2019. The shares were repurchased at an average price of €22.38 per share for a total consideration of €25 million. These repurchases were made as part of the €1 billion share buyback program announced on November 13, 2018.

![]()

The total number of shares repurchased under this program to date is 2,757,700 common shares for a total consideration of €61.7 million.

Based on the Company’s fundamentals with excellent Price to Sales of 0.43 and the fact that the company is buying back its own shares, we maintain our BUY rating on the shares of Ahold-Delhaize.

Disclosure:

I / We are long shares of SINOPEC as well as Ahold-Delhaize.

Last but not least, before taking any investment decision, always take your investment horizon and risk tolerance into consideration. Keep in mind that share prices do not move in a straight line. A Past Performance Is Not Indicative Of Future Results. Shares of emerging markets and commodity based companies might experience a higher volatility than the ones of developed market big-caps.

Yours sincerely,

Eric Panneflek